Introduction

The sports betting industry is undergoing a phase of deep transformation. Growth is no longer driven solely by geographic expansion or aggressive marketing. The market is becoming more complex: regulation is tightening, the share of live betting is increasing, and the role of technology and analytics is expanding. Competition is shifting away from marketing budgets toward product quality — including data processing speed, infrastructure resilience, the effectiveness of risk management, and the depth of personalization.

In 2025–2026, the industry’s development is shaped by three key factors:

- The clear dominance of online betting, which now accounts for roughly 75% of global wagering activity — driven primarily by mobile

- The rapid expansion of live betting, micro-markets, and same-game parlays (SGPs) within a single event

- The firm establishment of esports as a mainstream vertical within the betting ecosystem

To better understand these shifts, let’s explore both the global landscape and key regional nuances.

Global Market

The global sports betting market is estimated at approximately $112 billion in 2025. Over the long term, it is projected to grow to around $325 billion by 2035, with a compound annual growth rate of roughly 11%.

However, the headline figures tell only part of the story. What matters more is the structural shift taking place within the market. Growth today is not just quantitative but also qualitative. Products are becoming more sophisticated, while demands on technology and regulatory compliance continue to increase.

Regional GGR Breakdown

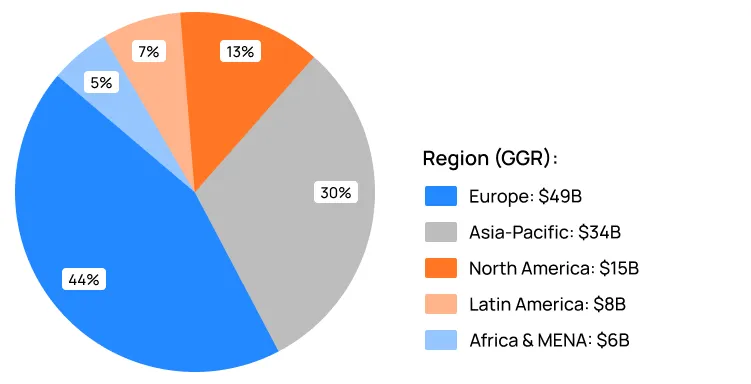

Fig. 1: Estimated global sports betting GGR distribution by region, 2025

Based on the estimated global GGR distribution for sports betting in 2025:

- Europe remains the largest market, accounting for approximately 40–44% of global GGR.

- Asia-Pacific is delivering the strongest growth, despite regulatory constraints in several countries.

- North America continues to expand steadily following the legalization wave in the United States.

- Latin America and Africaare the fastest-growing regions in terms of development pace.

At the same time, regulatory pressure is intensifying across mature markets: taxes are increasing, betting limits are being introduced, and player verification requirements are becoming more stringent. While this does not slow overall market growth, it is reshaping operator strategies — shifting the focus from scale to efficiency.

Live Betting, Micro-Markets, and SGPs

In recent years, live betting has become the primary driver of wagering volume. On some platforms, live accounts for up to 70–80% of total betting activity, while among leading operators it can generate around 80% of revenue.

What’s driving the growth

Micro-betting

Wagering on short in-game moments or micro-events — such as the next play, shot, point, foul, or ball out of play. Users can place dozens of bets within a single match. In more mature markets, particularly the U.S., micro-betting already represents a significant share of activity, with estimates reaching up to ~35% of all bets.

Same Game Parlays (SGPs)

Multiple bets within a single match. A “build-your-own” format combining outcomes, totals, and player stats. SGPs boost average revenue per user by increasing engagement and enabling a high number of combinations.

Prop bets (player and team stats)

Bets on individual player and team performance metrics — such as shots on target, aces, fouls, assists, or cards. Growth in prop markets is evident across most regions, but particularly in markets where sports are consumed as a data-rich media product, such as the U.S. and Europe.

How These Formats Are Reshaping the Economics of Betting Operators

- They increase betting frequency, with users placing significantly more bets within a single event

- They shift competition toward UX and speed — if odds updates lag, users quickly switch to alternative platforms

- They require more advanced risk management, with a greater number of markets and more potential points of exposure (e.g. arbitrage, latency issues)

- They are highly data-dependent: without high-quality data feeds and trading capabilities, micro- and live betting products break down

This leads to a broader conclusion: in 2025–2026, betting products increasingly resemble real-time data processing systems rather than simple odds boards.

Esports

In recent years, esports has evolved from a “youth-focused experiment” into a segment that is now shaping betting operator strategies.

Key metrics relevant for product and investment decisions:

- the global esports audience is expected to exceed 600 million in 2025, including around 318 million core viewers

- total esports industry revenue is estimated at approximately $1.8 billion

- the esports betting market is projected to reach around $2.8 billion in 2025 (up from ~$2.5 billion in 2024)

- approximately 74 million users placed online bets on esports during 2024

- the segment is showing strong growth even in mature markets — for example, the UK reported ~29% year-over-year growth

- the audience skews young: around 78% of esports bettors are under 35, with a predominantly male user base

Key Titles

In 2024–2025, the most actively bet-on esports titles included Mobile Legends: Bang Bang, Counter-Strike 2, League of Legends, and Dota 2. This matters not only for marketing, but also for trading: each title has its own match dynamics, event structure, and market logic.

Risks That Cannot Be Ignored

The primary risk is match-fixing. Esports is particularly vulnerable at the tier-2 level, where there is a high volume of tournaments, relatively low prize pools, younger teams, and weaker oversight mechanisms. This requires enhanced monitoring and close collaboration with tournament organizers.

As a result, mature esports betting in 2025–2026 consistently includes:

- betting anomaly detection and monitoring

- close cooperation with tournament operators

- restricting or removing markets where event integrity is uncertain

- well-calibrated limits and risk models

Regional Market Analysis

Europe: Maturity, Regulation, and the Fight for LTV

Europe holds the largest share of global betting revenue and remains the benchmark for "regulated markets". However, it is also where pressure is most pronounced: growth is slowing, while regulatory and operational requirements continue to intensify.

Market dynamics

- Europe accounts for approximately 38–44% of global sports betting GGR

- the largest markets include the UK, Italy, Germany, France, and Spain

- football dominates, representing up to ~75% of total betting volume in leading markets

- competition is intense: success depends not only on odds, but also on product quality, user experience, payments, and brand trust

Regulatory Pressure

Europe is moving toward a more restrictive regulatory model:

- deposit and staking limits

- expanded KYC/AML requirements

- affordability checks (particularly in the UK)

- increasing tax pressure (e.g. higher betting taxes in certain jurisdictions)

- restrictions on advertising and sponsorship

The impact is twofold: while parts of the gray market are being reduced, licensed operators are also losing some volume due to tighter restrictions. As a result, strategy is shifting toward efficiency — with greater focus on personalization, CRM, retention, and ARPU growth.

Outlook for 2025–2026

Growth in Europe is expected to remain moderate, but the region will continue to set industry standards:

- further development of live betting offerings

- expansion of bet builders and stat-driven markets

- ongoing technological optimization

- market consolidation, with stronger operators acquiring local players while weaker ones exit

CIS

The CIS betting market continues to show stable demand, particularly in the online segment, while operating under increasingly stringent regulatory conditions. Russia remains the largest market in the region, where online betting volumes continue to grow, although tax pressure is rising and transaction monitoring requirements are becoming more rigorous.

Market characteristics:

- a high share of live betting: among leading operators, live can account for over 70% of total turnover

- sports mix: football (~40–45%), combat sports (10–17%), esports (10–11%), and hockey (8–9%), with variations across countries

- a strong esports ecosystem (particularly Dota and CS), supporting continued growth in esports betting

Technological landscape

- mandatory digital identification and integration with state and banking systems

- active adoption of AI for fraud detection and risk management

- early rollout of micro-betting, requiring near real-time data synchronization and market pricing

- increasing use of automated blocking and behavioral scoring for suspicious activity

Outlook for 2025–2026

The regulated segment is expected to grow, driven by users’ increasing preference for online products. However, profitability will depend heavily on taxation and compliance costs. The winners will be operators that can:

- maintain platform stability and speed

- respond quickly to risk factors (e.g. multi-accounting, bonus abuse)

- deliver personalized offers without breaching regulatory constraints

- continue developing their esports segment

Asia-Pacific (APAC)

APAC represents the largest growth opportunity in terms of audience scale, but the region remains highly fragmented — ranging from strict prohibitions to selective market liberalization.

The key challenge is the prevalence of restrictions and gray markets. In many countries, betting is either illegal or heavily limited, yet demand persists — shifting to offshore operators, VPN access, and crypto-based platforms. At the same time, some jurisdictions are developing licensing frameworks and positioning themselves as regional hubs.

Where is the growth coming from?

Southeast Asia is seeing strong growth in the online segment, largely driven by the adoption of mobile payments. At the same time, the region has one of the strongest esports cultures globally, making esports a default expectation within the product for a significant share of users.

Australia: a distinct case

Australia is a mature market with strict regulation and limitations on online betting. This creates a paradox: restrictions on online live betting have contributed to the growth of the offshore segment.

Outlook for 2025–2026

APAC will remain the region with the highest long-term potential, but growth will be driven by:

- the expansion of localized licensing models

- mobile-first products and local payment solutions

- esports

- stronger RG frameworks as regulation catches up with the market

North America

Following legalization, the U.S. has become the primary hub for product innovation — including same-game parlays (SGPs), micro-betting, media integration, and the standardization of data feeds and trading.

By early 2025, legalization had expanded across dozens of states. In 2024, total betting handle reached $149.9 billion, with GGR at $13.78 billion (+25% year-over-year). The market is highly competitive, with a small number of major operators controlling the majority of the online segment.

This is also where product standards are being established most rapidly:

- SGPs as a core feature

- micro-betting as a dedicated, high-frequency offering

- “betting + media” as a unified funnel — including dedicated broadcasts, embedded odds, and in-play betting during live viewing

- a strong focus on data: official feeds, minimal latency, and automated trading

Canada and Mexico

Canada is demonstrating a successful model of gradual liberalization, particularly at the provincial level. Mexico is notable for its combination of strong football culture and the influence of U.S. sports; additionally, the 2026 FIFA World Cup is expected to drive increased engagement across the region.

Latin America

In 2025–2026, Latin America is one of the most dynamic growth regions. Brazil is at its center.

As of January 1, 2025, a regulated betting market has been introduced there. Dozens of licenses have been issued, with a tax rate of approximately 18% of GGR. The market is estimated at around $4.7 billion in 2025. Football remains dominant (accounting for up to 94% of betting audience interest), though esports and other verticals are gaining traction.

Brazil is notable not only for its scale. It also sets a new regulatory benchmark: strict KYC requirements, local data storage, and enhanced payment controls. As a result, operators often need to adapt their infrastructure specifically to meet local requirements.

Other markets in the region

Latin America is a patchwork of regulatory regimes. Colombia was the first to legalize online betting back in 2016 and is often cited as a successful regulatory model. Today, the market includes 20+ licensed operators, with around 68% of the population participating in gambling activities, and sports betting accounting for roughly 47% of total gambling GGR. However, in 2025, Colombia introduced a temporary 19% VAT on player deposits (until year-end), which has faced criticism and may push some users back to the gray market. Argentina operates under a decentralized model, where each province licenses independently. In major provinces such as Buenos Aires, the market is open, but there are no truly nationwide operators. The total gambling market is estimated at around $6.4 billion in 2025, with online accounting for approximately $1.57 billion. While sports betting is popular, the market has a unique feature: alongside football, horse racing betting remains significant — a legacy of the country’s long-standing racing culture — accounting for up to $1.5 billion. Peru legalized betting in 2024, introducing a tax structure of 12% of GGR plus an additional 1% of turnover allocated to social programs. Chile and Uruguay are in the process of updating their regulatory frameworks, but for now, these markets remain largely gray, with many users betting on offshore platforms that are not strictly enforced against.

Outlook for 2025–2026

The market could potentially double in revenue over the next few years, but success will depend on:

- local payment solutions (e.g. PIX in Brazil as a de facto standard)

- strong mobile-first UX

- marketing discipline and responsible advertising (as regulators react quickly to excessive promotion)

- technological upgrades, including AI-driven scoring, risk engines, and personalization

Africa and MENA

Africa is showing some of the highest growth rates globally, driven primarily by mobile adoption.

- hundreds of millions of users are engaged in betting, with the market estimated at around $17.6 billion in 2025

- average annual growth is ~17%

- key markets include Nigeria, South Africa, Kenya, Ghana, and Uganda

- mobile dominates: around 91% of bettors use their phones

The key "catalyst" in Africa has been the rapid rise of mobile payment systems. Services such as M-Pesa (Kenya), MTN Mobile Money (Ghana, Nigeria), and OPay (Nigeria) have enabled users without traditional bank accounts to participate in digital commerce and betting. Today, around 91% of African bettors use mobile devices. Very often they place micro-bets: average stake sizes can be just a few dollars or less, but with very high frequency. Mobile money has made deposits and withdrawals instant and accessible even in rural areas with basic connectivity. At the same time, the widespread availability of affordable smartphones — particularly from Chinese manufacturers — has brought online betting apps and platforms to millions of new users.

The market is characterized by low average ticket sizes and high betting frequency. Success depends heavily on accessibility:

- lightweight apps optimized for low-end Android devices and poor connectivity

- support for USSD/SMS in certain markets where it remains critical

- instant payouts to mobile wallets

MENA

Historically, gambling has been prohibited across most Middle Eastern countries due to religious norms. However, 2025 marked a potential turning point: the UAE (Dubai) issued the region’s first betting license — for the Play971 project, supported by operator Wynn. The platform is primarily targeting tourists and expatriates, operating under the supervision of the newly established regulator, the GCGRA. This represents a notable precedent for the Gulf region. Elsewhere in MENA, full legalization has yet to materialize, but indirect developments are emerging. In 2025, Morocco introduced a 30% tax on winnings from foreign online casinos (plus an additional 2% social contribution), effectively acknowledging offshore gambling activity among its citizens and seeking to capture part of the value. In parallel, as part of preparations for the 2025 Africa Cup of Nations, Morocco has invested in sports infrastructure, partly funded through lottery revenues. Potentially, it was laying the groundwork for future betting market reforms. Saudi Arabia and Qatar remain firmly opposed to gambling, although both continue to invest in international gaming and entertainment assets. Overall, MENA remains a relatively small segment of the global market. Most local users who wish to bet rely on offshore platforms, often accessed via VPN. At the same time, surveys suggest underlying demand: in the UAE, around 36% of residents consume betting-related content on social media, approximately 27% report placing bets online (likely via offshore platforms), and 17% do so several times per week. The most popular sports in the region include football, cricket (driven by the South Asian diaspora), basketball, as well as traditional formats such as horse and camel racing. If regulatory barriers are eased, the UAE’s iGaming market alone is estimated to have the potential to reach $8–10 billion annually.

Outlook for 2025–2026

Africa is expected to sustain strong growth and become an increasingly competitive arena for both international and local operators. In MENA, progress is likely to remain gradual: one or two additional jurisdictions may introduce regulated models if early initiatives prove viable.

Technology Trends and Product Evolution in Betting

In 2025–2026, most meaningful product differentiation is driven by engineering and analytics capabilities.

Data feeds, latency, and ultra-low-latency streaming

For live betting and micro-markets, minimizing latency across the entire chain is critical: event → calculation → odds update → bet acceptance. The target range is 1–2 seconds, and the industry is investing heavily in:

- direct partnerships with data providers

- push-based protocols (e.g. WebSockets)

- edge infrastructure closer to both data sources and end users

- application and CDN optimization

Automated trading and AI-driven models

Trading is shifting from reactive, manual processes to proactive, model-driven systems. Probabilities are continuously recalculated in real time, taking into account the full context of the match. This reduces pricing errors and mitigates exposure to arbitrage. A separate layer of complexity comes from SGPs: operators require advanced engines capable of accurately modeling correlations between outcomes and delivering instant pricing.

Big Data and Personalization

Retention is becoming the primary KPI, especially in markets where marketing is constrained. A CDP-driven approach enables operators to:

- predict churn

- deliver personalized offers and market recommendations

- optimize bonus allocation and economics

- simultaneously support responsible gambling (RG) by identifying risky behavior

Scalability and Microservices

The technical architecture of betting platforms is also evolving. Previously dominated by monolithic systems, top players are now transitioning to microservices. By breaking the platform into multiple independent services (bet placement, pricing, registration, payments, etc.), operators can scale specific components under peak load — improving both performance and resilience.

KYC/AML, Biometrics, and Fraud Prevention

Regulators are requiring deeper verification of both users and financial flows. At the same time, risks such as deepfakes and document forgery are increasing, driving the need for more advanced automated validation. While these measures can negatively impact user experience, they are unavoidable. In mature markets, success depends on balancing fast onboarding with rigorous compliance controls.

Outlook for 2025–2026: What Comes Next

Bringing these trends together, several practical conclusions emerge.

Global growth will continue

By 2026, global sports betting GGR could approach $150 billion. It should be driven primarily by the U.S., Brazil, Africa, and the continued migration of users to online channels.

Live and micro-betting will become the standard

The share of live betting will continue to grow toward dominance, reaching up to ~75% of total bets in some markets. Micro-betting will account for a significant share of total bet volume and will require new levels of infrastructure sophistication.

Regulation will intensify

Particularly in Europe and other mature markets, with tighter affordability checks, advertising restrictions, betting limits, and stricter compliance requirements. New markets are likely to “learn from Europe” and embed RG frameworks from the outset.

Consolidation is inevitable

This is an increasingly expensive industry: licenses, taxes, data contracts, compliance, and product development all raise the barrier to entry. As a result, M&A activity will accelerate — stronger operators will acquire market share and technology, while weaker players exit.

Esports will solidify as a core vertical

Growth will continue, but so will the cost of integrity failures. By 2025–2026, esports will become a mandatory component of the product offering for operators targeting younger audiences.

What Investors and Operators Should Do: A Practical Checklist

To ensure this overview translates into action, here is a set of key questions to address in 2025–2026.

For investors

- In which markets is growth driven by regulation, and where is it sustained by gray-market activity?

- How high are compliance and data infrastructure costs in the target jurisdiction?

- Does the project have the technical capability to scale live and micro-markets without compromising UX?

- How robust is the risk engine (bonus abuse, arbitrage, multi-accounting, speed of limit enforcement)?

- Is there a clear strategy for esports?

For operators and product teams

- Can you maintain latency levels that are competitive in live betting?

- Do you have an SGP / bet builder with a reliable correlation model?

- How mature is your CDP/CRM setup (segmentation, churn prediction, personalized offers)?

- How long does KYC take, and what is the drop-off rate at each stage?

- How quickly can you respond to threats such as arbitrage, professional bettors, syndicates, and fraud?

- Is your product ready for local payment methods and regional specifics (e.g. PIX, vouchers, mobile money, USSD)?

If you’re unable — or simply don’t want — to address all of these questions internally, you can always reach out to the 01.tech betting module team. We’ve already solved them.

Conclusion

By 2025–2026, the sports and esports betting industry is at the peak of a major transformation. On one hand, there is continued geographic expansion and an influx of new users; on the other, increasing pressure from regulation, responsibility requirements, and an accelerating technology race. For investors, the sector remains highly attractive: a large and growing market where meaningful share can still be captured — particularly in high-growth regions such as Africa, Latin America, and APAC. However, market entry now requires more than capital. Success depends on understanding local dynamics and being prepared for rising compliance complexity.

For those already operating in the space, the key message is clear: innovation and user experience are decisive. The future belongs to operators that can deliver a highly interactive, personalized, and secure betting experience.

The industry has always been closely tied to technology, and that connection is only strengthening. In many ways, betting operators are evolving into fintech companies built around entertainment. Those that adapt quickly to this new reality will capture the greatest upside in the years ahead, as the industry continues to grow, evolve, and remain an integral part of the global sports ecosystem.

Share: